Expect an invitation first. Ally Bank distributes prescreened offers worldwide, and each envelope or email includes a unique access code that unlocks the online application.

You need that code because Ally’s system rejects unsolicited submissions, protecting existing customers and keeping approval odds high for those selected.

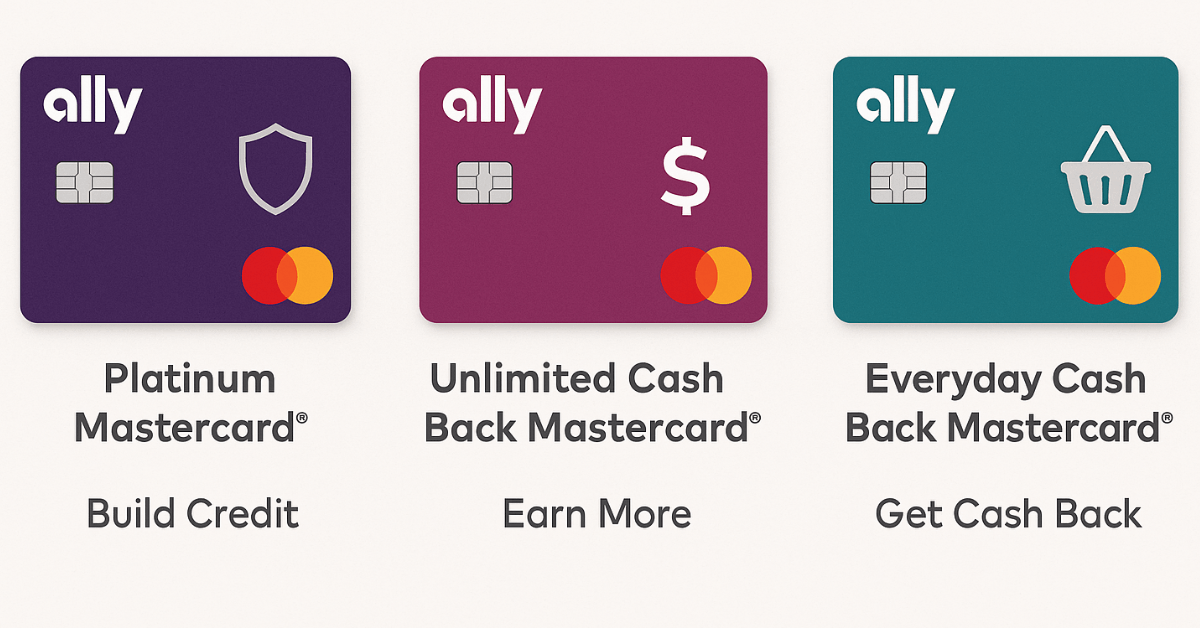

Three Distinct Ally Cards, One Invitation Per Card

Each invitation references a specific product, so you cannot swap cards at checkout. Knowing every option ensures you recognize the card tied to your code and decide quickly.

Ally Platinum Mastercard®

A credit‑building tool with no annual fee, no rewards, and automatic line‑increase reviews after five timely payments.

Ally Unlimited Cash Back Mastercard®

A flat 2 percent cash back rate on every purchase, no foreign transaction fee, and no annual fee, giving straightforward earnings worldwide.

Ally Everyday Cash Back Mastercard®

Unlimited 3 percent cash back at grocery stores, gas stations, and drugstores and 1 percent elsewhere. The annual fee ranges from $0 to $39, determined by your credit profile.

Choosing Based on Credit Standing

Selecting the right invitation begins with an honest assessment of your current score range.

- Credit builders (580–669): You benefit most from the Platinum Mastercard because approval standards are flexible, and no security deposit applies.

- Fair‑to‑good credit (670–739): Everyday Cash Back becomes attractive if recurring grocery and fuel spending dominates monthly budgets.

- Good‑to‑excellent credit (740+): Unlimited Cash Back delivers maximum flat earnings, yet alternative 2 percent cards worldwide often add welcome bonuses and introductory APR periods, so compare before proceeding.

Eligibility Signals Before the Mail Arrives

Understanding the traits that trigger an offer helps you gauge your chances. Ally typically screens mid‑tier credit profiles, stable income histories, and low delinquency records.

You do not need an Ally deposit account, yet keeping balances elsewhere will not exclude you. Credit builders and moderate spenders receive priority because the issuer targets underserved segments rather than premium travelers.

Step‑by‑Step Online Application

A clear sequence keeps the process efficient and minimizes errors that could trigger rejection.

- Gather documents—valid ID, proof of income, and the invitation letter containing the access code.

- Navigate to the Ally application portal—follow the URL printed in the offer or scan the provided QR code.

- Enter the access code—type it exactly as shown; the system auto‑populates card details.

- Complete personal information—input current address, contact number, and employment data. Maintain consistency with your credit report to avoid verification delays.

- Review rates and fees—confirm the annual fee, variable APR range, and rewards summary displayed on screen.

- Consent and submit—agree to electronic disclosures, then click “Submit.” A soft pull usually becomes a hard pull only if the decision is favorable.

- Track status—expect an email decision within sixty seconds in most cases; complex profiles could require manual review lasting up to ten days.

Factors Influencing Approval Odds

Ally assesses three pillars. It's important that you understand what these pillars are.

- Payment history length — Longer histories with punctual repayments build trust.

- Utilization ratio — Keeping balances below thirty percent signals responsible management.

- Recent inquiries — Multiple hard pulls within six months may flag risk even with a prescreened offer.

Meeting those benchmarks tilts the algorithm toward approval yet remains no guarantee; drops in income or emergent delinquencies since the screening date can reverse eligibility.

Understanding Annual Fees and Interest Ranges

Annual fees differ by product and sometimes by applicant for the Everyday card. Variable APR spans 17.99 percent to 29.99 percent.

Ally adjusts the exact rate after approval based on your credit characteristics, so reading the digital disclosures before confirmation protects you from unpleasant surprises.

Rewards Mechanics Without Earning Caps

Both rewards cards impose no ceiling on cash back, a notable perk at the 3 percent tier for groceries and gas.

Cash back posts after each statement cycle and never expires, allowing you to accumulate balances until an ideal redemption time. Redemptions begin at one cent, letting you sweep earnings as statement credits whenever cash flow matters.

Missing Features Compared to Global Competitors

You sacrifice two common perks:

- No sign‑up bonus—Many worldwide 2 percent cards offer $200‑equivalent welcome cash after modest spend thresholds.

- No introductory APR—Competitors often grant 12‑ to 15‑month zero‑interest periods on purchases or balance transfers, easing large upfront expenses.

Decide if immediate rewards out‑weigh the absence of those features or if an alternative issuer would stretch value further.

Pros and Cons at a Glance

Weigh these clear advantages and limitations to decide if this card fits your financial needs and spending habits.

Advantages:

- Access codes lower approval barriers for fair credit profiles.

- No penalty APR or over‑limit fees improve cost predictability after mistakes.

- Free FICO access supports continuous credit monitoring.

- Zero foreign transaction fees support worldwide travel spending.

Limitations:

- Invitation requirement restricts timing; you cannot apply on demand.

- Variable APR tops out higher than many mainstream cards, increasing interest costs if balances roll.

- Lack of sign‑up incentives reduces short‑term value.

- Everyday card’s annual fee—up to $39—diminishes net 3 percent earnings for low spenders.

Alternatives Worth Comparing

When an invitation sits beside other pre‑approved offers, weigh Ally against these widely available choices:

- Wells Fargo Active Cash®—2 percent everywhere, welcome bonus, and fifteen‑month 0 percent APR period.

- Citi Double Cash®—1 percent at purchase and 1 percent at payment, with global merchant acceptance and no annual fee.

- Capital One SavorOne®—3 percent on dining, entertainment, streaming, and groceries worldwide, plus a one‑time bonus and no foreign fee.

Evaluating those cards ensures you maximize lifetime earnings instead of grabbing the first prescreened envelope that arrives.

Decision Checklist Before Clicking “Apply”

Use this quick filter to confirm the invitation aligns with personal goals:

- Projected monthly spend in eligible bonus categories exceeds $500.

- Ability to pay statements in full avoids high variable APR charges.

- No pending mortgage or auto applications that would suffer from another hard inquiry.

- Alternative cards with sign‑up bonuses fail due to stricter credit thresholds.

If each condition reads “yes,” completing the online application makes practical sense.

Conclusion

Receiving an Ally access code delivers a streamlined path toward credit building or uncomplicated cash rewards, especially for mid‑tier profiles worldwide.

Nevertheless, the absence of sign‑up bonuses and introductory APRs means you should pause and compare open‑access options before committing.

Align the card’s strengths—unlimited earnings, low fees, and minimal penalties—with your current credit objectives and spending habits to ensure the invitation becomes a genuine advantage rather than a missed opportunity.